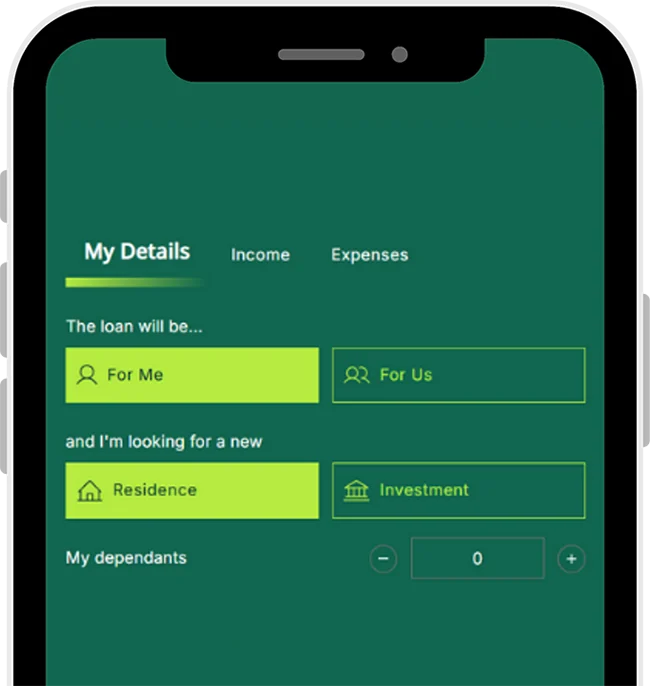

In 2025, there are more ways than ever to get into the market, even if your savings are limited. Whether you’re a first home buyer, an upgrader, or buying with family support, the right lender and structure can help you move sooner.

What’s the Standard Deposit in 2025?

Traditionally, lenders prefer a 20% deposit. But in today’s lending environment, many approved buyers can secure a home loan with:

5%

deposit

through standard low-deposit loans

2%

deposit

through government-backed schemes

0%

deposit

using a family guarantor

The right option depends on your income, eligibility, and lender policy.

Who Can Buy With Less Than 20%?

At Flenley Financial Group, we regularly help:

First home buyers

with limited savings

Young professionals

Young professionals renting while saving

Families leveraging

guarantor support

Single parents

eligible for the Family Home Guarantee

Buyers using grants

to reduce upfront costs

Even if you don’t have the full 20%, you still have options.

Understanding LMI (Lenders Mortgage Insurance)

Borrowing more than 80% of a property’s value usually means LMI but that doesn’t mean a huge upfront cost.

Many lenders let you capitalise the LMI into the loan

Professionals (healthcare workers, teachers, etc.) may be eligible for LMI waivers

The cost of waiting to save 20% can often exceed the cost of LMI

Our Fee Structure:

No Cost to You

We’ve built exclusive relationships with over 340 lenders.

When you apply through Flenley, the lender pays us — not you.

No hidden fees. No upfront charges.

Just expert advice focused on what’s best for your financial future.