Choosing between a fixed or variable rate can feel overwhelming — especially with interest rates shifting in 2025. Whether you’re a first-time buyer, investor, or refinancing your current mortgage, understanding the pros and cons of each option is key to making a confident decision.

At Flenley Financial Group, we help clients compare both fixed and variable rate home loans across 340+ lenders, tailoring recommendations based on your financial goals and lifestyle.

What’s the Standard Deposit in 2025?

Traditionally, lenders prefer a 20% deposit. But in today’s lending environment, many approved buyers can secure a home loan with:

What Is a Fixed Rate Home Loan?

A fixed rate loan means your interest rate is locked in for a set period — typically 1 to 5 years.

Key Benefits:

Predictable monthly repayments

Protection from rate rises

Easier budgeting for short- to mid-term plans

Things to Watch Out For:

Less flexibility (limits on extra repayments and redraws)

Break costs may apply if you end the loan early

You might miss out on rate drops

What Is a Variable Rate Home Loan?

With a variable rate loan, your interest rate can change based on market conditions.

Key Benefits:

More flexible (extra repayments, redraws, and refinancing)

Protection from rate rises

Often lower fees than fixed loans

Things to Watch Out For:

Repayments can increase without warning

Harder to budget if rates rise

Requires more active loan management

Split Loans: Best of Both Worlds?

A split loan allows you to fix part of your loan and leave the rest variable.

Why Some Borrowers Choose This:

Stability from the fixed portion

Flexibility from the variable side

Can suit uncertain interest rate climates (like 2025)

Fixed vs Variable in 2025: What We’re Seeing

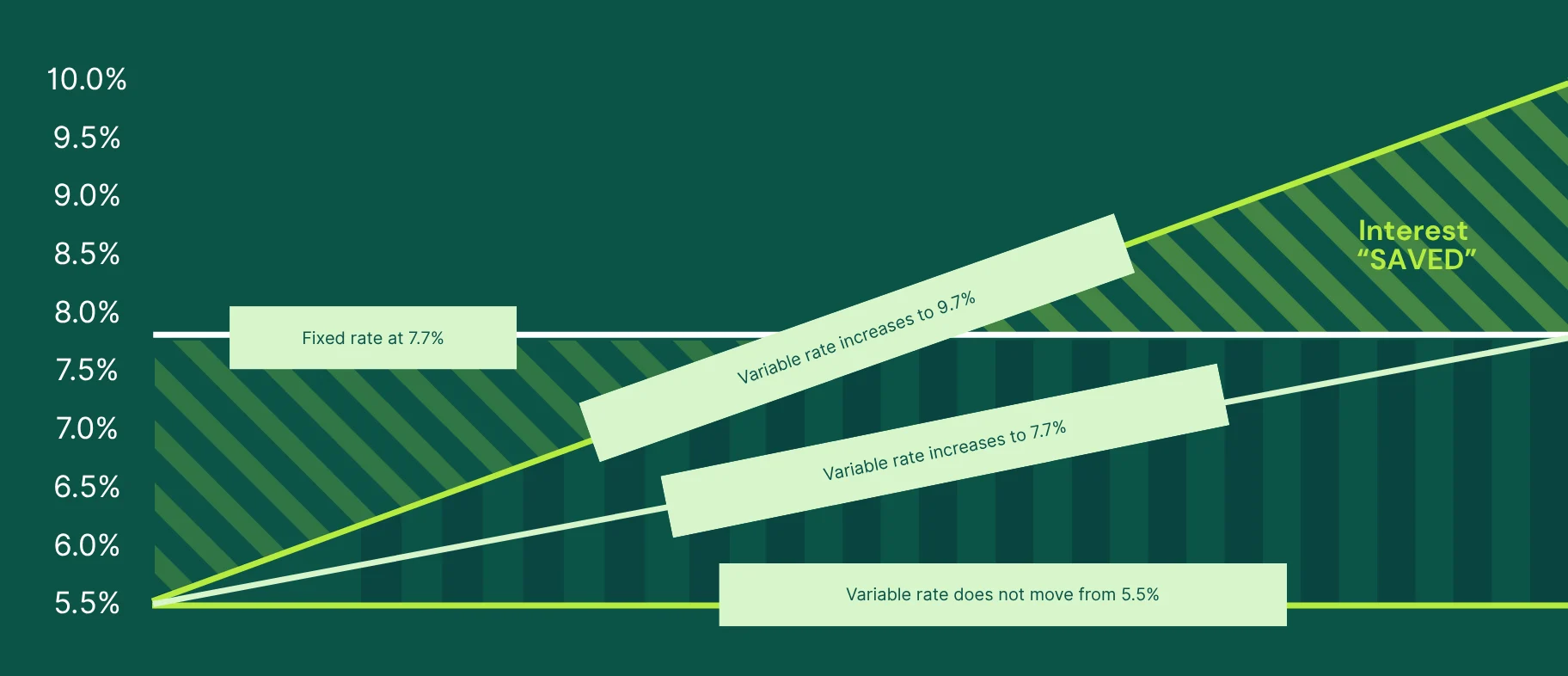

Let’s say you take out a $300,000 home loan on a 30-year term. Now imagine you’re comparing two options: a variable rate starting at 5.7% and a fixed rate locked in at 7.7% for five years. If interest rates stay flat at 5.7% during that five-year period, fixing at 7.7% could end up costing you significantly more about $30,000 in additional interest. That’s a tough pill to swallow, especially if the market stays steady.

An example of different interest rate scenarios for the first five years of a 300,000 home loan

Now let’s say rates rise gradually from 5.7% to 7.7% over those five years. Even then, fixing would still cost you around $15,000 more in interest. For the fixed rate to actually break even with the variable rate, the variable rate would need to jump sharply reaching about 9.7% after five years. Only then would the total interest paid equal the cost of fixing at 7.7%.

This is why choosing between fixed and variable isn’t just about guessing where rates will go, it’s about how long you plan to hold the loan, your risk tolerance, and how much flexibility you want.

Our Fee Structure:

No Cost to You

We’ve built exclusive relationships with over 340 lenders.

When you apply through Flenley, the lender pays us — not you.

No hidden fees. No upfront charges.

Just expert advice focused on what’s best for your financial future.

Fixed, variable, and split loan options tailored to your goals

Clear advice without bank bias

No client fees

Help with refinancing, first-time purchases, and low deposit loans

Personalised structuring based on your income, goals, and life stage

Still Deciding Between Fixed or Variable?

We’ll help you understand which loan structure makes the most sense for your situation — whether you’re buying your first home or refinancing in a rising market.