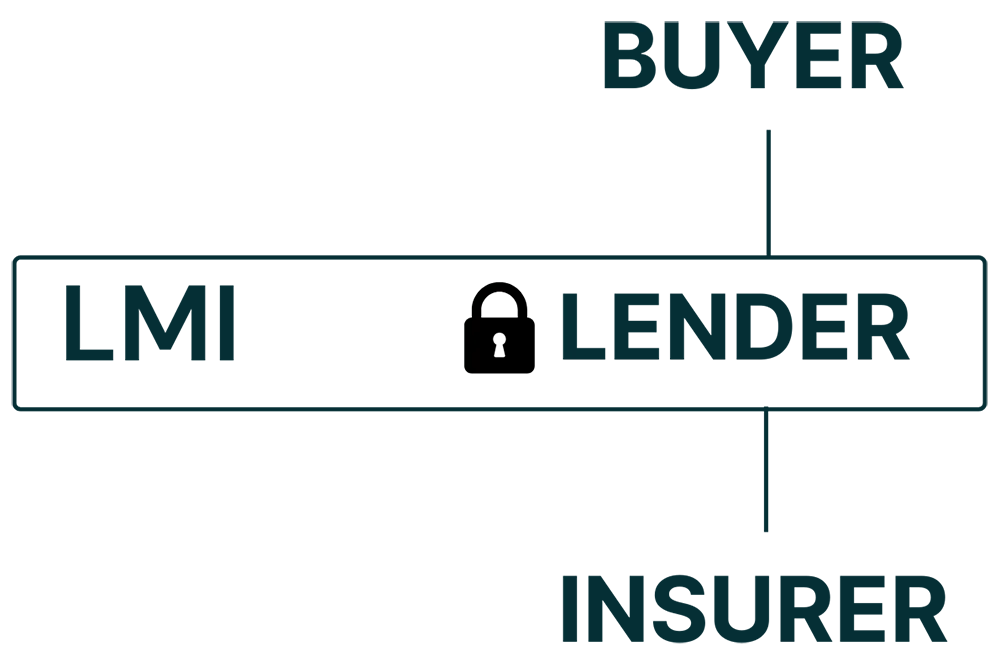

Lenders Mortgage Insurance (LMI) is a one-off insurance premium charged by lenders when your deposit is less than 20% of a property’s value. It protects the lender — not you — if you default on your loan.

If you’re borrowing more than 80% of the property’s value (which is called a high LVR loan), you’ll typically be required to pay LMI.

Who Pays LMI and Why?

LMI is most common among:

First home buyers with small deposits

Borrowers using 5–15% deposits

Applicants without a guarantor

Self-employed or casual income earners without full documentation

While it can cost thousands, LMI allows you to enter the market sooner without waiting years to save a 20% deposit.

Can You Avoid Paying LMI?

Yes — here’s how:

Save a 20% deposit

Use a guarantor loan (family member offers equity)

Qualify for LMI waivers (available to doctors, lawyers, accountants, teachers, and healthcare professionals with strong credit)

Use government schemes like the First Home Guarantee, which allows eligible buyers to buy with 5% deposit and no LMI

Is Paying LMI Ever Worth It?

Yes — in many cases, paying LMI can be smarter than waiting years to save 20%.

Get into the market sooner

Benefit from property price growth while you own, not rent

Start building equity faster

At Flenley Financial Group, we help you weigh up the cost of LMI vs the cost of delaying.

Our Fee Structure:

No Cost to You

When you work with Flenley, the lender pays us — not you.

✔ No client fees ✔ No hidden costs ✔ Just expert advice on whether LMI is worth it for your situation